Achieving effective consumer representation: a study of the UK Payments Sector

Sarah O’Neill Independent Researcher, Queen Margaret University, Edinburgh EH21 6UU.

Carol Brennan Honorary Reader, Queen Margaret University, Edinburgh, EH21 6UU.

Sally Chalmers Honorary Senior Lecturer, Queen Margaret University, Edinburgh, EH21 6UU.

Jane Williams Senior Lecturer, Queen Margaret University, Edinburgh, EH21 6UU.

---

Abstract

Purpose

As financial institutions seek to innovate in a competitive landscape, consumer representation, providing a strong voice for consumers and encouraging organisational responsiveness, is increasingly valued and seen as a route to restoring confidence, improving marketing effectiveness and new product development. Research in this area is limited and there is a lack of managerial guidance. This study contributes through the development of a model for effective consumer representation.

Design / methodology / approach

A review of existing knowledge and empirical data collection in the financial services payments sector underpins model development. Data gathering included face-to-face and online interviews with consumer representatives and a round-table discussion involving consumer representatives and industry professionals.

Findings

Culture, people and process underpin the model. Organisations should build a culture that puts consumers at the centre and seek transparency. Representatives should have the competence, knowledge, skills and qualities to reflect consumer views, and to instil confidence in consumers and consumer organisations. Tailored training, processes which rebalance power between industry and consumer, adequate resources and appropriate structures are needed. Guidance for organisational leaders is provided and applicable to the wider financial sector internationally. There is scope to develop the model for other regulated and non-regulated sectors.

Originality

Consumers should be at the heart of organisational decisions. The data highlights the value of listening to the ‘consumer voice’ and provides evidence-based solutions relevant to complex regulatory sectors. Further research is highlighted.

Keywords

Consumer representation, consumer voice, consumer engagement, consumer panels, financial services, payments.

Article classification

Research paper

Introduction

Financial services institutions are under pressure to innovate as their competitive landscape undergoes a seismic shift (Estelami, 2012) and trust is rebuilt. Increasing active participation and involvement of consumers has been identified as a route to restoring confidence and driving best practice in the financial sector (European Parliament and the Council of the European Union, 2017) and developing new products (Mohammad et al, 2016. Martovoy et al, 2012). Indeed, financial services marketers cite understanding of the consumer environment as one of the top factors which could substantially improve marketing effectiveness (Hinshaw, 2005)

Consumer representatives are one route through which this input is provided. In recent years there has been rising interest in the importance of consumer representation, in regulated industries in the UK and globally (UK Regulators Network, 2017; Consumer Council for Water, 2020; Consumer Protection, 2020; Lodge, 2016; Essential Services Access Network, 2017; Consumers Health Forum of Australia, 2020, Tambini, 2012). The engagement and participation of citizens, consumers and customers addresses the shortcomings of hierarchical, expert-driven control associated with the technocratic regulatory state. Ensuring that the consumer interest is represented is particularly important in complex markets such as financial services, which may be difficult for consumers to understand, access and navigate (Estelami, 2012; FSCA-OECD, 2019; European Commission, 2016; Financial Conduct Authority, 2020; Financial Conduct Authority, 2016) and where poorly informed decisions can lead to major financial and emotional impact on consumers (Financial Services Consumer Panel, 2019; Citizens Advice, 2016; European Commission, 2016; Office of Fair Trading 2008). The payments sector is one element of financial services which has received increased attention from academics in consumer research (Hirshman, 1979; Raghurst, 2006; Penz and Sinkovics, 2013) and marketing (Raghubir and Corfman, 1999, Lawson and Todd, 2003).

Delivering effective consumer representation is, however, not straightforward. This is partly due to a lack of research into consumer involvement and representation models and there is considerable scope for improvement in taking the consumer interest into account (Consumers International, 2020; Franceys and Gerlach, 2011). This article seeks to advance knowledge and understanding of consumer representation. It draws on research undertaken with the financial payments market to explore how consumer representation can best be achieved in complex technical markets. It is proposed that the resulting lessons have wider relevance to inform consumer representation models across other sectors.

Literature review

Consumer representation is defined as the formal mechanisms for the representation of consumer interests within the public and private sector. Consumer representatives voice consumer perspectives, often in an advisory capacity, and may take part in the decision-making process on behalf of consumers. Effective consumer representation contributes to better decision-making as representatives can bring knowledge and experience that enables officials to develop a clear understanding of the elements of a successful solution and the likely consequences (Consumer Protection, 2020; Consumers Health Forum of Australia, 2020). The concept of consumer representation is not new. Consumer rights set out in 1962 by President John F. Kennedy included the right to be heard. This has since developed into ‘consumer influence and representation’, one of eleven internationally recognised consumer principles used by consumer organisations to define the most important needs of consumers which should be taken into account in decision-making (Consumers International, 2016; UK Regulators Network, 2017). Other consumer principles are access, information, education, safety, redress, inclusivity, protection of economic interests, sustainability, e-commerce rights and privacy.

There is surprisingly little academic literature focused on consumer representation with much of what is available being policy-focused. In contrast there is a significant literature spanning a number of different disciplines on consumer engagement (Andersson et al, 2011; Franceys and Gerlach, 2011). While the terms consumer representation and consumer engagement are often used interchangeably, consumer engagement is focused on a broader approach to consumer voice which includes engaging directly with consumers themselves by, for example, encouraging the active participation of consumers in the planning, delivery and evaluation of services as well as undertaking consumer research.

Consumer representation has effects at the organisational, regulatory and market level. It makes organisations more directly responsive to consumers (Tambini, 2012), ensuring that products and services better meet the needs of consumers (CAA Consumer Panel, 2019; Consumer Focus, 2011). It assists the development of regulatory regimes, improving the quality of regulatory decision-making and supporting the appropriateness of regulatory interventions (Consumers International, 2020; Consumer Focus, 2011). At the market level, consumer representation increases public trust (Scottish Legal Complaints Commission Consumer Panel, 2018; Consumer Focus, 2011). Effective representation of the consumer interest can help rebalance the asymmetry of power and bring clarity about issues faced by consumers (Office of Rail and Road, 2019). It promotes trust and confidence in the relevant sector; responds to consumer needs, particularly those of vulnerable and low-income groups; and leads to good outcomes both for consumers and for the sector itself (Consumer Protection, 2020; Consumers Health Forum of Australia, 2020).

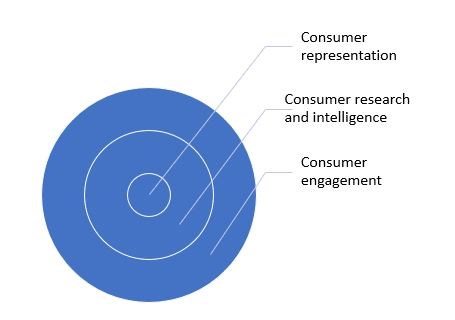

This section focuses on investigating alternative terms for consumer representation, and provides an analysis of structural requirements for achieving effective consumer representation. A range of terms are used to describe the involvement of consumers in organisations. Consumer engagement can involve the active participation of members of the public, service users or customers in service planning, delivery and evaluation (Andersson et al, 2011; Consumer Focus Scotland, 2011). It also includes ‘indirect’ engagement with consumer bodies, carrying out consumer research and gathering consumer intelligence, such as complaints data and satisfaction surveys, on an ongoing basis (Coppack et al, 2014). A relationship between consumer representation and engagement is shown at Figure 1.

Figure 1: Relationship between consumer representation and consumer engagement

The concept of ‘consumer voice’ has been considered in a range of settings, including regulation (National Consumer Federation, 2020), healthcare (Fox, 2008), employee relations (Yamaguchi, 2005), essential services (Essential Services Access Network, 2017), services marketing (Lacey, 2012) and public services (Simmons and Brennan, 2016). Across these, ‘voice’ is seen as providing an opportunity for people to get their point of view across to decision-makers (Bies, 1987); provide their ideas, suggestions, concerns or opinions in order to improve organisations (Morrison, 2011); be communicated with, consulted and have a say (Dundon et al, 2004); and be listened to (Essential Services Access Network, 2017; Consumer Focus, 2011).

Organisational outcomes associated with collaborative consumer voice include the creation of consumer trust, legitimacy for organisational decisions and increased engagement, all of which facilitate the delivery of organisational goals (Essential Services Access Network, 2017). Voice is particularly important in regulated sectors which provide essential services and where customer choice is limited (National Consumer Federation, 2020; Essential Services Access Network, 2017).

The term consumer engagement is used in literature to refer to consumer voice and consumer representation. Most of the recent literature on consumer voice sees this as consumer engagement (Lodge, 2016; Essential Services Access Network, 2017; Sustainability First, 2016; Consumer Focus Scotland, 2011; Andersson et al, 2011; Coppack et al, 2014; Perceptive Insight, 2016), but, while consumer representation and consumer engagement cover similar ground, consumer engagement is broader than, and encompasses, consumer representation (see Figure 1).

Consumer engagement conceptualisations include those which provide both active participation of members of the public, service users or customers, in service planning, delivery and evaluation (National Consumer Federation, 2020; Andersson et al, 2011; Consumer Focus Scotland, 2011), and those which deliver ‘indirect’ engagement with consumer bodies, carrying out consumer research and gathering consumer intelligence, such as complaints data and satisfaction surveys, on an ongoing basis (Coppack et al, 2014; CAA, 2019).

Engagement approaches include those aimed at ensuring consumer rights and representation, those facilitating stakeholder engagement with government and regulators (through consultative processes or the existence of particular committees) and project focused citizen participation and deliberation (Fung, 2015; UK Regulators Network, 2017).

Public participation is widely regarded as a form of democracy, allowing individuals to play a part in decisions affecting them which are made by others. Central to this idea of participation is the notion of power. The more power is shared the greater the level of citizen participation and empowerment (McKeever, 2013). The concept of public participation provides a range of roles for consumers. These range from informing consumers to consulting them, involving them, and collaborating with them, and then to ultimately empowering them (see Figure 2) by placing the decision in their hands (Perceptive Insight, 2016). Participation has been seen as an important value in consumer contexts in which consumer empowerment and self-efficacy are stressed (Williams et al, 2020).

Figure 2: Public participation spectrum (IAP2)

Adapted from the International Association for Public Participation, 2014.

Participation is viewed as a process for influencing decisions, plans, or policies that directly affect one's community, government, and personal or public life. It is one facet of societal and institutional inclusion, and its denial is a form of exclusion. Participation can be considered to be on a continuum, where there are increasing levels of interaction with other decision-makers, influence over the outcome, and power to determine the outcome (Gius, 2018). Democracy theorist Carole Pateman has described three points along this continuum: pseudo-participation, where one has no influence or power over the outcome; partial-participation, where one has influence but no power; and full participation, where one has full power over the outcome. Like dignity, participation is highly relational. A simple framework captures many of the potential dynamics between the parties involved (decisionmakers, people affected by a decision, and any third parties such as advocates or facilitators): decisions can be made or implemented with people, to people, or for people. While there are times when doing things to or for people might be appropriate and affirm dignity, the with approach is often framed as the participatory ideal (Pateman, 1970 p53). Participation therefore is an important element in consumer representation.

The following section considers structural requirements for effective consumer representation. Organisational culture, people and processes are identified below as important to the provision of effective consumer representation and a number of existing models for consumer representation are identified and critiqued.

In terms of culture, it is important that the wider culture within organisations is focused on consumers and is (and is seen to be) receptive to and welcoming of consumer views. Consumer representation is least effective when it is a tick-box exercise. To avoid the perception that consumer representation is just window dressing, there should be clarity about the role of the consumer representative and how their input will be used (Financial Services Consumer Panel, 2019; Consumer Focus, 2011). Consumer representatives should have actual involvement in decision making and be viewed as equal participants (McAuley, 2016).

Consumer input on decisions should be valued at an early stage, and an attitude which allows sufficient time for consumer representatives to provide meaningful input into policy making and decisions should exist. Cultural approaches should reject consumer input as being viewed as a ‘rubber stamp’ (UK Regulators Network, 2017).

A culture of access, transparency and evaluation should exist to enable consumers to respond flexibly and rapidly to any new problems that arise. Consumer representatives should have access to high quality research, market intelligence and other evidence, to gain insight into the consumer experience of markets (CAA, 2019; Office of Rail and Road, 2019; Sustainability First, 2016). Arrangements for consumer representation should also be open and transparent. The impact of consumer representation should be measured and publicly reported (ORR Consumer Expert Panel, 2020a), clearly demonstrating how it has influenced policy and decision-making (UK Regulators Network, 2017; Coppack et al, 2014). Indicators should be developed to measure the success of consumer representation arrangements, and their effectiveness should be periodically reviewed (Coppack et al, 2014).

Although it has been identified that financial institutions gain from co-operation with external partners in developing successful innovations, this co-operation does bring problems with it (Martovoy, 2014) which include the risk of selecting wrong partners, costs associated with co-operation, bureaucracy, conflicts in the alignment of objectives (Martovoy, 2014). Consumer representation too has inherent limitations. It cannot ensure that the views of all consumers have been taken into account. One representative cannot possibly represent the views and interests of every individual within a diverse range of consumers. It is important to recognise and consider the views and needs of different consumer cohorts – for example, older/younger consumers; those in different socio-economic groups, and those living in different geographical areas (Consumer Focus, 2011; Coppack et al, 2014; Sustainability First, 2016; UK Regulators Network, 2017). Organisations should take a proactive approach to engaging consumer representatives, in order to attract a diverse range of people, rather than just ‘the usual suspects’ (Coppack et al, 2014; Essential Services Advisory Network, 2017) and target hard-to-reach and vulnerable groups through outreach work (UK Regulators Network, 2017). In addition, those individuals who represent the consumer interest must have the competence, knowledge and qualities required to do so effectively (National Consumer Federation, 2020; Consumer Focus, 2011; UK Regulators Network, 2017; Union des Consommateurs, 2009).

Key principles for the appointment of consumer representatives to government and industry bodies set in Australia (Commonwealth Consumer Affairs Advisory Council, 2005) include appointment on merit: demonstrable consumer affairs expertise, a capacity and willingness to consult with consumer organisations, and a knowledge of, or the ability to acquire knowledge of, the industry/issues involved. They should also have links to relevant consumer organisations, should be independent of industry and government, with no conflicts of interest, and should have the confidence of the consumer. Other principles for appointing effective consumer representatives include competence, independence, representativeness, and accountability (Union des Consommateurs, 2009).

Payments are often referred to as the ‘plumbing’ of financial services (Committee on Exiting the European Union (CEEU), 2017) and finding consumer representatives with the right blend of technical expertise in addition to understanding how to represent the consumer interest is not an easy task (2018). As a payments industry response, Bacs has appointed consumer representatives to provide a strong, independently minded executive that is focused on being consumer-led, to build consumer focused networks, develop a research programme for the sector, and reach out beyond the ‘usual suspects’ (Bacs, 2017).

Effective consumer representation requires the establishment of a range of processes. An ‘effective mechanism for ensuring that consumer interests are “heard” and acted upon’ (Western Australia Department of Consumer and Employment Protection, 2006, p2.) is needed. Consumer representatives must have confidence in the process so that they feel they are genuinely being listened to and can influence decision-making rather than shouting into a black hole (Consumer Focus, 2011; McAuley, 2016)

Appointment processes which are consistent with good corporate governance are those which are clear, transparent and accountable (Commonwealth Consumer Advisory Committee, 2005). An appropriate range of potential candidates should be sought as a lack of diversity and relying too heavily on the “usual suspects” may be an issue (Coppack et al, 2014; Essential Services Access Network, 2017). Consumer representatives tend to be middle income, middle aged, educated professionals, rather than lay representatives or those whose voice is vital - the ignored, isolated and invisible (Franceys and Gerlach, 2011). Attempts should therefore be made through appropriate routes to reach such groups, in order to bring in fresh voices (UK Regulators Network, 2017).

Training is needed (Bacs, 2017). Potential consumer representatives may lack the necessary resources, expertise and capacity to take on the role (Essential Services Advisory Network, 2017). The imbalance between consumer representatives and other players, especially in relation to complex and technical issues, can place them at a significant disadvantage (Financial Services Consumer Panel, 2013). Potential consumer representatives may therefore require significant support in terms of administration, capacity building, technical support and ongoing training, to allow them to take on the role (Coppack et al, 2014).

Organisations should show that they value the input and time given by representatives, by publicly reporting consumer input in board minutes and other documents, including changes which have been implemented as a result of their contribution (ORR, 2020; UK Regulators Network, 2017; Coppack et al, 2014).

Consumer representatives have a range of resource needs. Access to good quality research data is needed to support the views they put forward (CAA, 2019; Consumer Focus, 2011; Sustainability First, 2016). They also require financial support, through both payment and reimbursement of expenses, in order to carry out their role effectively (Bacs, 2017). ‘No person should be expected to sacrifice their normal salary in order to contribute as a consumer representative. Apart from the lack of equity in such a position, it devalues the role of the representative.’ (Commonwealth Consumer Affairs Advisory Committee, 2005, p13).

Three broad models of consumer representation identified within a regulatory context could have wider application (UK Regulators Network, 2017; Essential Services Advisory Network, 2017). Each of these has advantages and disadvantages and there is no definitive best approach. The most effective will depend on the sector and context (UK Regulators Network, 2017; Sustainability First, 2016).

Model 1: ad hoc consultation or engagement with external consumer groups While consumer bodies may have a key role to play under this model, the extent to which they can represent consumers’ interests may be limited. Lack of resources and/or technical expertise may force them to focus on everyday issues directly relevant to consumers, at the expense of more complex issues where the long-term consumer interest is less clear cut. Research on consumer representation within the financial services sector (Financial Services Consumer Panel, 2009) found, for example, that few consumer bodies specialise in financial services, and those who do may not always be able to respond to consultations due to limited resources and time.

Model 2: appointing representatives to advisory panels and groups within the regulator Government departments, regulatory bodies and businesses may have some form of expert consultative committee to consider consumer issues. For example, the Financial Services Consumer Panel advises and challenges the Financial Conduct Authority, which is legally required to consider its representations; these are taken very seriously by the regulator (Financial Services Consumer Panel, 2019).

Under this model consumer panels can provide independent, expert advice; become involved at an early stage; have a deep understanding of complex sector-specific issues; and can be seen as a trusted ‘critical friend’, giving them greater influence over decision-making. They may not, however, be seen as entirely independent, there may be the risk of ‘capture’; are resource intensive; and may find it difficult to ensure they represent ‘real’ consumers (Coppack et al, 2014; Essential Services Advisory Network, 2017).

Model 3: engagement through the regulated company itself This model may be used by regulators in relation to price controls - for example, the Customer Forum, which negotiates directly with Scottish Water (UK Regulators Network, 2017). Additionally, companies may appoint consumer representatives directly to their boards (Essential Services Advisory Network, 2017). This approach can encourage companies to be more consumer focused; allow ongoing trusted input and challenge from a different perspective; and may increase company credibility. It does, however, pose difficulties for representatives, particularly volunteers, in devoting sufficient time to fully participate. They may also not have sufficient expertise to deal with complex issues. Paid representatives appointed by the company may not be seen as independent. (Essential Services Advisory Network, 2017).

The above review has provided an insight into what comprises successful consumer representation, through the identification of key roles; cultural, people and process requirements, and through a critique of existing models. This framework informed, and was further developed through, research conducted within the financial sector. The output ultimately provides a model for effective consumer representation offered in this paper.

Methodology

To empirically inform the development of the model, qualitative data was gathered from consumer representatives, expert informants and other stakeholders in an iterative cycle to provide rich and deep engagement with the subject matter. Thematic analysis was used to identify and categorise naturally occurring themes from a series of semi structured telephone and online interviews. Further depth was achieved through a process of reality checking at a round-table event which included a sample of the interviewees plus other stakeholders. The research explored views on the role of consumer representation; possible performance criteria for consumer representation; and what skills, knowledge and qualities effective consumer representatives would need.

The data presented below was gathered as part of a research project with Bankers Automated Clearing Services Ltd (Bacs) in 2017 on what good consumer representation in the payments sector should look like, and how this might best be achieved, within a changing technologically-driven landscape.

At the time of the research Bacs was responsible for direct debit payments and the Current Account Switching Service (CASS) and was subject to calls to ensure that consumers’ interests are appropriately represented. This was deemed important following the establishment of the current account switching service in 2013 which aimed to increase competition by enabling consumers to easily switch retail banking. The importance of ensuring good consumer representation in this sector was highlighted as retail banking is "often people’s first experience of financial services and can offer a gateway to further financial inclusion” (Financial Inclusion Commission, 2015, p. 26). Since the research was conducted, Bacs has been replaced by Pay.UK.

Methods

Methods included telephone interviews, an online survey using open-ended questions and a round table discussion.

Twelve semi-structured telephone interviews were carried out between June and July 2017 with expert informants from across the UK. These informants had extensive expertise regarding the issue of consumer representation either within financial services or more widely which gave them insight into the subject being researched. While statistical generalisation was not the aim, the research sought to achieve a balanced sample by including interviewees who were or had been consumer representatives in the financial sector, advice bodies, independent experts, and consumer representative groups. Telephone interviews were used to gather data from these professionals who were geographically spread across the UK. Interviews lasted an average of 60 minutes.

To extend data gathering reach an online questionnaire was also sent to a group of eight stakeholders. Three participants provided online responses.

Interview data was professionally transcribed and uploaded along with the online questionnaire responses to Nvivo, coded and analysed. We concluded that data saturation was reached as no new codes were added during the last few interviews.

Further iteration was achieved through the discussion of findings and recommendations at a round-table event which also provided a reality check for final recommendations.

Findings and discussion

This section provides and discusses the key findings from the research. These are organised by topic with data being drawn from all research participants.

1. General views on consumer representation

Research participants valued their involvement in consumer representation, seeing it as a unique role which provided a real insight for organisations. The aim of consumer representation was seen to be ensuring that when key decisions are being made, the consumer perspective is brought to bear. Bringing that understanding; advocating for consumer interests; and influencing decision making by facilitating a more consumer-centred focus were seen as key to success.

Participants at the round-table event suggested that a consumer-focused culture was central to successful consumer representation. Effective consumer representation relied on the organisation demonstrating a willingness to listen to consumer representatives and take into account their views. This may involve a culture change throughout the organisation, towards adopting a more consumer-centric approach, which recognises the importance of customers, and addresses any resistance to consumer input.

Consumer engagement should be embedded across an organisation rather than being viewed as a ‘bolt on’. As one round-table participant observed: “it is imperative that boards stop considering their needs as separate from consumer needs, but rather recognise that the consumer needs are the board and business’s needs”.

Consumer representation in financial services was viewed as crucial: while organisations within the industry were seen to put forward a combined voice, the consumer voice was less coherent. It was recognised, however, that there were specific challenges to be faced in ensuring effective consumer representation within the payments sector. Consumer organisations had not to date significantly engaged with payments issues, partly due to the technical complexity involved and the pace of technological change. Moreover, payments were not necessarily seen by consumers or consumer organisations as a directly consumer facing issue. Consideration therefore needs to be given to how to arouse interest and motivate potential consumer representatives in relation to payments issues.

Consumer representation was viewed as different from consumer engagement; the latter was seen to be more about organisations involving individual consumers in the services they deliver. Some interviewees highlighted that effective consumer representation does not start or end with attendance at a meeting; there is a need to engage consumers using a variety of methods. These might include the organisation adopting a partnership approach by reaching out to consumer groups, and using digital consumer engagement channels, in order to reach new voices, better reflecting the diversity of consumers.

2. Views on consumer representation models

Interviewees were asked for their views on two models: the appointment of individual consumer representatives to an organisation’s governing body; and a collective consumer forum within the payments sector. Both were seen to have strengths and disadvantages.

On the former, some thought that commercial organisations tend to see their own priorities as more important than those of consumers and interviewees expressed concern that one consumer representative on a board may be quite isolated. Interviewees also acknowledged that it was ‘tricky’ for a single representative to take account of the diverse needs of all consumers. As one said: ‘while it would be lovely to have representatives of different consumer constituencies, I imagine there is a size of board after which it becomes unwieldy’.

They also felt, however, that having consumer representatives on the board might, however, motivate the board to listen more effectively to the consumer perspective, and to think about things differently. There was a recognition that a consumer representative could have a catalytic impact, encouraging the organisation to take consumer interests into account, driving wider engagement, and ensuring that the voices of more excluded consumers are heard.

It was also recognised that other board members may be able to contribute to a consumer perspective. Some suggested that all board members should be trained in consumer issues, which might provide an opportunity to leave their organisational view behind and contribute as individuals.

While the single representative model had limitations, it could be an important part of a wider strategy to engage with consumers. Consultation with consumer bodies was seen as important to ensure that a broader perspective is reflected during discussions. Consumer representatives should also be involved in designing and developing the organisation’s consumer engagement strategy. Some suggested that consumer representatives could become ambassadors, reaching out to their own networks in developing the engagement strategy. A note of caution was expressed about this, however, consumer representatives should not be expected to conduct the engagement with consumers themselves. This is a substantial task which should be carried out by staff within the organisation and with consultants commissioned to focus on particular aspects of activity.

For the purposes of the research a consumer was defined as anyone, whether an individual or an SME, that uses of or would like to use, the services provided. While interviewees thought that the interests of small and micro enterprises were often similar to those of consumers, they had reservations about whether a single representative would be able to cover both perspectives. While separate representation might be difficult within a smaller board, this could be delivered via a consumer panel. Likewise, there was a strong consensus that the interests of price comparison organisations and intermediaries were not well aligned with those of individual consumers: these bodies should therefore also be separately represented.

While it was seen as an expensive option, the second model (a collective consumer forum) was thought to be effective in representing different consumer perspectives, ensuring that a diverse range of views were heard. A strong consumer panel, with different areas of expertise around the table, was seen to be important. Limitations included the cost, difficulties in attracting a diverse range of representatives, and that sometimes the size of group forums can be too large to achieve useful progress. It has been found that a consumer panel of six to twelve experts works effectively (Financial Services Consumer Panel, 2020; Civil Aviation Authority Consumer Panel, 2020; Office of Rail and Road Consumer Expert Panel, 2020b; Scottish Legal Complaints Commission Consumer Panel, 2020). Some felt that having consumer representatives on the board was important even where there was also a collective forum. At the Civil Aviation Authority, the Chair of the Consumer Panel regularly attends Board Meetings (Civil Aviation Authority Consumer Panel, 2020) to represent the views of the Panel and at the Office of Rail and Road, a member of the Board chairs the Consumer Expert Panel (Office of Rail and Road, 2020b). Both approaches ensure that the panels have clear insights to the strategic direction of the organisations and can ensure that the consumer voice is heard at the highest level.

Interviewees were asked whether consumer representatives should be appointed as individuals, or as representatives of an organisation, regardless of the model chosen. Some felt that a degree of pragmatism was needed, depending on the person and organisation concerned. Most favoured individual appointments, on the basis that this would help to ensure that the appointee did not simply represent the views of their organisation. It was recognised, however, that working for an organisation would give them access to research and evidence that may not otherwise be available to them.

3. What would good consumer representation in the payments sector look like?

Participants highlighted a range of cultural, people and process factors as underpinning good consumer representation in the payments sector. These largely supported those which emerged from the literature review (see Table 1).

Table I : Factors required to achieve effective consumer representation

[Adapted for web - for full table please download full paper]

Principle: Culture

| Factor highlighted by research participants | Participant comments | Supporting literature |

|---|---|---|

| Involving representatives at an early stage |

Mitigates against a perception that their views are not being taken seriously. Ensures early identification and consideration of consumer. |

UK Regulators Network, 2017 |

| Being seen to have influence - making a difference |

Builds consumer trust in the process. Ensures consumer confidence that they are genuinely being listened to. Organisations to show they value consumer representative input and time by publicly reporting consumer input and consequential changes made in board minutes and other documents. |

Consumer Focus, 2011 McAuley, 2016 UK Regulators Network, 2017 Coppack et al, 2014 |

Principle: People

| Factor highlighted by research participants | Participant comments | Supporting literature |

|---|---|---|

| Reflecting the diversity of consumer interests, so far as possible | Organisations to be proactive, undertake outreach to target hard-to-reach and vulnerable groups and consult effectively with consumer representatives. | Graham, 2016 Coppack et al, 2014 Essential Services Access Network, 2017 National Consumer Council, 2008 UK Regulators Network, 2017 Consumer Focus, 2011 UK Regulators Network, 2017 Union des Consommateurs, 2009 |

| Recruiting the right person to the consumer representative role |

Specifically in:

|

As above |

Principle: Process

| Factor highlighted by research participants | Participant comments | Supporting literature |

|---|---|---|

| Access to financial support | Remuneration is needed as organisations cannot rely on goodwill and volunteering and need to demonstrate the value consumer representative expertise. This also makes it clear consumer representatives are expected to take the role seriously and helps to widen the pool of potential individuals and organisational applicants. | Commonwealth Consumer Affairs Advisory Committee, 2005 |

| Access to good quality research data | Important to supporting the views put forward by consumer representatives. | Consumer Focus, 2011 Sustainability First, 2016 Graham, 2016 Coppack et al, 2014 |

| Access to technical and administrative support | Administrative support and technical training and support needed. | As above |

A model for effective consumer representation

The literature review highlighted the importance to good consumer representation of having the right culture, people and processes in place. The research findings confirmed these principles providing further rationale and elucidation. These are presented in a model for effective consumer representation in Figure 3.

Figure 3: A model for effective consumer representation. Principles and underpinning factors

| Culture |

|---|

| Open and transparent |

| Consumer focused |

| Receptive and welcoming of consumer views |

| People |

|---|

| Competence, knowledge, skills and qualities to reflect consumer views |

| Consumers and consumer organisations have confidence in the person |

| Independent of industry and free of conflicts of interest |

| Process |

|---|

| Appointment process is transparent and accountable in accordance with good corporate governance |

| Financial resources to support representatives |

| Training and support |

These principles are to some extent mutually dependent and reinforce each other. Processes which facilitate consumer representation work best within a culture that is receptive and open to consumer input. Likewise, having the right culture is likely to lead to a desire to invest in good consumer representation processes, and in people who will be effective consumer representatives. It is the dynamic of culture, people and process that makes consumer representation effective.

Culture

Where an organisation’s culture is open and transparent, receptive and serious about putting the consumer at its heart, consumer representation can have an impact. This means seeing consumers not simply as another group of stakeholders, but as the success metric of an organisation: good consumer outcomes should be synonymous with the organisation’s success.

Organisations should be able to show where they have listened effectively to the consumer voice and made changes. They should be transparent when views are rejected, giving clear reasons why the input has not been addressed. Holding open board meetings, publishing meeting minutes, consumer research and the outcomes of key debates through dedicated internet pages can help create transparency.

People

The capabilities which interviewees identified as necessary for effective consumer representatives echoed those in the literature. These include: access to good quality evidence to help them build their case; relationship building with stakeholders; involvement at an early stage; the ability to represent diverse consumer interests; and relevant knowledge, skills and expertise.

Process

Interviewees noted that while consumer representation is ‘essential’, it is ‘difficult to get right’. In order to ‘get it right’, consumer representatives must be supported by processes which allow them to be effective. Good processes include: transparency of criteria for selection; responsible appointment processes; the application of good governance rules; financial resources; training support; and involvement of consumer organisations.

Managerial implications

In establishing how good systems of consumer representation might be developed, within the payments sector and more widely, leaders should pay attention to the following.

Culture

Consumers should be put at the heart of all decision making, with consumer values central to the organisation’s culture and strategy. Consumer representation should be viewed as one, albeit crucial, element, of an organisation’s broader consumer engagement, communication and advocacy strategy, within a consumer-focused culture. The role and way of working of consumer representatives should be transparent and influential. In order to promote transparency, key representative objectives, performance information, minutes of meetings and annual reports should be made publicly available. The effectiveness of consumer representation should be evaluated. Clear, measurable objectives should be set for the organisation’s approach to consumer engagement and consumer representation.

People

It is important to appoint consumer representatives who have the necessary competence, knowledge, skills and qualities to reflect consumer views. They should have the confidence of consumers and consumer organisations. They should be supported through such training and capacity building as they require.

Process

Consumer representation structures should be adequately resourced to rebalance power between the industry and the consumer. Sufficient resources should be allocated to attract and pay consumer representatives, enable research to be carried out, and provide administrative support. Consumer representation should ideally be structured to include both board and collective forum representatives, supplemented by direct outreach to consumer organisations.

Directions for future research

The research contained in this paper suggests several further research strands. Firstly, this research focuses on the payments sector. Research into the applicability of the model developed in this paper in other sectors would develop its usefulness and reveal whether similar principles could be effectively applied elsewhere. Secondly, this research identified that, while there is a significant body of academic research on consumer engagement, the research on consumer representation has tended to be policy focused and this gap needs to be addressed. Further academic research into the role, requirements and contextual settings for good consumer representation is needed. Thirdly, where literature on consumer representation is present it relates primarily to a regulatory context. More work is needed into the establishment of good consumer representation in non-regulatory settings. Fourthly, the model developed is based on research conducted in the UK. Further research to establish its applicability internationally is required.

Bacs. (2018), ‘The consumer conundrum (external PDF): ensuring effective representation in financial services’ (accessed 6 July 2020)

Bacs. (2017),’Consumer representation in financial services (external PDF): a Bacs discussion paper’ (accessed 9 June 2020)

Bies, R. (1987), ‘Beyond ‘voice’: the influence of decision-maker justification and sincerity on procedural fairness judgments’. Representative Research in Social Psychology. Vol 17 No.1, pp. 3-14.

Brennan, C., Williams, J., O’Neill, S. and Chalmers, S. (2017), ‘Consumer Representation in Financial Services (external PDF): report into consumer representation in the payment sector’ (accessed 11 March 2020)

CAA Consumer Panel. (2020) ‘Consumer Panel members’ (accessed 19 June 2020)

CAA Consumer Panel. (2019) ‘Civil Aviation Authority (CAA) Consumer Panel Annual Report 2018-2019’ (accessed 9 June 2020)

CAA. (2019), ‘Civil Aviation Authority UK Aviation Consumer Survey Wave 8 (Autumn 2019)’ (accessed 9 June 2020)

Citizens Advice. (2016), ‘Consumer detriment: counting the cost of consumer problems (external PDF)’, London: Oxford Economics. (accessed 10 March 2020)

Committee on Exiting the European Union (CEEU), (2017), ‘Payments Systems and Services Sector Report (external PDF)’, House of Commons, London (accessed 13 July 2020)

Commonwealth Consumer Affairs Advisory Council (CCAAC). (2005), ‘Principles for the appointment of consumer representatives: a process for governments and industry’, Canberra: Commonwealth of Australia.

Consumer Council for Water. (2020), ‘Consumer representation' (accessed 1 June 2020)

Consumer Focus. (2011), ‘Regulated Industries and Consumers (external PDF)’ (accessed 10 March 2020).

Consumer Focus Scotland, (2011), ‘Consumer Engagement in Decision Making: best Practice from Scottish Public Services (external PDF)’ (accessed 10 March 2020)

Consumers Health Forum of Australia, (2020), ‘Consumer representation – the big picture’ (accessed 1 June 2020)

Consumers International, (2020), ‘Do consumer rights and needs matter? (accessed 8 June 2020)

Consumers International, (2016), ‘Consumer protection: why it matters to you. A practical guide to the United Nations guidelines for consumer protection’ (accessed 8 June 2020)

Consumer Protection, (2020), ‘What is consumer representation?’ (accessed 1 June 2020)

Coppack, M., Jackson, F. and Tallack, J., (2014), ‘Involving consumers in the development of regulatory policy (external PDF)’, UK Regulators Network (accessed 10 March 2020)

Dundon, T., Wilkinson, A., Marchington, M., and Ackers, P., (2004), ‘Changing Patterns of Employee Voice: case studies from the UK and Republic of Ireland’, Journal of Industrial Relations, Vol. 46, No.3, pp. 298–322

Essential Services Access Network, (2017), ‘How can the consumer voice be better heard in the regulation of essential services? (external PDF)’ ESAN Paper and Conference Report (accessed 13 July 2020)

Estelami, H., (2012), Marketing Financial Services, Dog Ear Publishing, Indianapolis, IN.

European Commission, (2016), ‘Consumer vulnerability across key markets in the European Union’ (accessed 13 July 2020)

European Parliament and the Council of the European Union, (2017), ‘Regulation (EU) 2017/826 of the European Parliament and of the Council, on establishing a Union programme to support specific activities enhancing the involvement of consumers and other financial services end-users in Union policy-making in the area of financial services for the period of 2017-2020’ Official Journal of the European Union (accessed 13 July 2020)

Financial Conduct Authority, (2020), ‘Using payment service providers’ (accessed 7 June 2020)

Financial Conduct Authority, (2016), ‘Access to financial services in the UK; Occasional paper 17 (external PDF)’ (accessed 13 July 2020)

Financial Inclusion Commission, (2015), ‘Financial Inclusion: improving the financial health of the nation (external PDF)’ (accessed 10 March 2020)

Financial Services Consumer Panel, (2020), ‘Who is on the panel’ (accessed 19 June 2020)

Financial Services Consumer Panel, (2019), ‘Annual report 2018/19 (external PDF)’ (accessed 7 June 2020)

Financial Services Consumer Panel, (2013), ‘Consumer representation at EU level (external PDF)’ (accessed 13 July 2020)

Financial Services Consumer Panel, (2009), ‘Consumer responsibility: the Financial Services Consumer Panel response to Discussion Paper 08/5’. London: FSCP

Franceys, R. and Gerlach, E., (2011), ‘Consumer involvement in water services regulation’, Utilities Policy, Vol. 19, No. 2, pp. 61-70, (accessed 10 March 2020)

FSCA-OECD, (2019), ‘Financial Education of the Future: summary record (external PDF) - International Conference on Financial Education, Cape Town, South Africa’ [Accessed 7 June 2020].

Fung, A., (2015), ‘Putting the Public Back into Governance: the Challenges of Citizen Participation and Its Future’, Public Administration Review, Vol. 75, No. 4, pp. 513-522

Gius, A.M., (2018), ‘Dignifying Participation’, N.Y.U. Review of Law & Social Change, Vol. 42. No. 1, pp. 45-91

Hinshaw, M., (2005), ‘A survey of key success factors in financial services marketing and brand management’, Journal of Financial Services Marketing, Vol. 10, No.1, pp. 37-48

Hirschman, E.C., (1979), ‘Differences in consumer purchase behaviour by credit card payment system’, Journal of Consumer Research, Vol. 6, No. 1, pp. 58-66

International Association for Public Participation, (20140, IAP2’s Public Participation Spectrum (accessed 11 March 2020)

Lacey, R., (2012), ‘How customer voice contributes to stronger service provider relationships’, Journal of Services Marketing, Vol. 26, No.2, pp. 137-144

Lawson, R. and Todd, S., (2003), ‘Consumer preferences for payment methods: a segmentation analysis’, International Journal of Bank Marketing, Vol. 21, No. 2, pp. 72-79

Lodge, M., (2016) (Ed.), ‘Customer Engagement in Regulation. Centre for Analysis of Risk and Regulation: discussion paper No 82 (external PDF)’ (accessed 10 March 2020)

Martovoy, A., Kutvonen, A., Mention, A. and Torkkeli, M., (2012), ‘Open innovation in banking services: advantages and disadvantages’, a paper presented at the XXIII International Society for Professional Innovation (ISPIM) Conference, Action for Innovation – Innovating from experience, Barcelona, Spain

Martovoy, A. (2014), “Advantages and disadvantages of open innovation: evidence from financial services”, Mention, A.-L. and Torkkeli, M. (Eds.), Innovation in Financial Services: a dual ambiguity, Cambridge Scholars Publishing, Newcastle upon Tyne, pp. 259-294

McAuley, T., (2016), ‘Consumer engagement in regulation (external PDF): what does good practice look like?’ Lodge, M. (ed) Customer Engagement in regulation, Centre for Analysis of Risk and Regulation: discussion paper No 82 (accessed 10 March 2020)

McKeever, G., (2013), ‘A ladder of legal participation for tribunal users’. Public Law. Vol. Winter, pp 575 – 598

Mohammad, G., Nejad, D., Martovoy, A. and Mention, A.L., (2016), ‘Patterns of new service development processes in banking’, International Journal of Bank Marketing, Vol. 34, No. 1, pp. 62-77

Morrison, E., (2011), Employee Voice Behaviour: integration and directions for future research, The Academy of Management Annals. Vol. 5, No. 1, pp. 373–412

National Consumer Council (NCC), (2008), ‘Putting People into Public Services’

National Consumer Federation. (2020). Consumer voice’(accessed 9 June 2020)

Office of Fair Trading, (2008), ‘Consumer detriment: assessing the frequency and impact of consumer problems with goods and services (external PDF)’, Office of Fair Trading (accessed 10 March 2020)

Office of Rail and Road, (2019), ‘Measuring up - Annual rail consumer report’ (accessed 9 June 2020)

Office of Rail and Road (ORR) Consumer Expert Panel, (2020a), ‘Consumer Expert Panel: how we work’, available from (accessed 9 June 2020)

Office of Road and Rail (ORR) Consumer Expert Panel, (2020b), ‘Consumer Expert Panel members’ (accessed 19 June 2020)

Pateman, C., (1970), Participation and democratic theory, Cambridge University Press, Cambridge

Penz, E. and Sinkovics, R.R., (2013), ‘Triangulating consumers’ perceptions of payment systems by using social representations theory: a multi-method approach’, Journal of Consumer Behaviour, Vol. 12, No. 4, pp. 293-306

Perceptive Insight, (2016), ‘Customer Engagement Methods and Examples of Best Practice: report for NIE Networks (External PDF)’ (accessed 10 March 2020)

Raghubir, P. and Corfman, K., (1999), ‘When do price promotions affect pretrial brand evaluations?’ Journal of Marketing Research, Vol. 36, No. 2, pp. 211-222

Raghubir, P., (2006), ‘An information processing review of the subjective value of money and prices’, Journal of Business Research, Vol. 59, No. 10, pp. 1053-106

Scottish Legal Complaints Commission Consumer Panel,(2020), ‘Consumer Panel members’ (accessed 29 June 2020)

Scottish Legal Complaints Commission Consumer Panel, (2018), ‘Consumer principles: applying the consumer principles to legal services – a tool for legal professionals and regulators’ (accessed 9 June 2020)

Simmons, R. and Brennan, C., (2016), ‘User voice and complaints as drivers of innovation in public services’, Public Management Review, Vol. 19, No. 8, pp 1085-1104 (accessed 13 July 2020)

Sustainability First, (2016), ‘Consumer, Citizen and Stakeholder Engagement and Capacity Building in the Energy and Water Sectors (external PDF): final discussion paper’ (accessed 10 March 2020)

UK Regulators Network, (2017), ‘Consumer Engagement in Regulatory Decisions (external PDF)’ available from (accessed 13 July 2020)

Union des Consommateurs (UDC), (2009), ‘Consumer Representation: recognition criteria’ available from (accessed 10 March 2020)

Western Australia Department of Consumer and Employment Protection (WADCEP), (2006), ‘Consumer representation on boards and committees: a guide for consumers ’ (accessed 10 March 2020)

Williams, J., Gill, C., Creutzfeldt, N., and Vivian, N., (2020), ‘Participation as a framework for analysing consumers’ experiences of alternative dispute resolution (external PDF)’, Journal of Law and Society, Vol. 47, No. 2, pp. 271-297

Yamaguchi, I., (2005), ‘Effective interpersonal communication in Japanese companies under performance-based personnel practices’, Corporate Communications: An International Journal, Vol.10, No.2, pp. 139-155

Acknowledgements

The data presented in this paper was gathered as part of a research project funded by Bacs as part of Pay.UK. The authors of this paper would like to express their gratitude to Simon Hanson for his assistance with recruiting participants during the data collection phase. The authors particularly want to thank Faith Reynolds for her guidance during the project.